Prof. Dr. Markus Meier

Leibniz Institute for Baltic Sea Research Warnemünde (IOW)

E-Mail: markus.meier@io-warnemuende.de

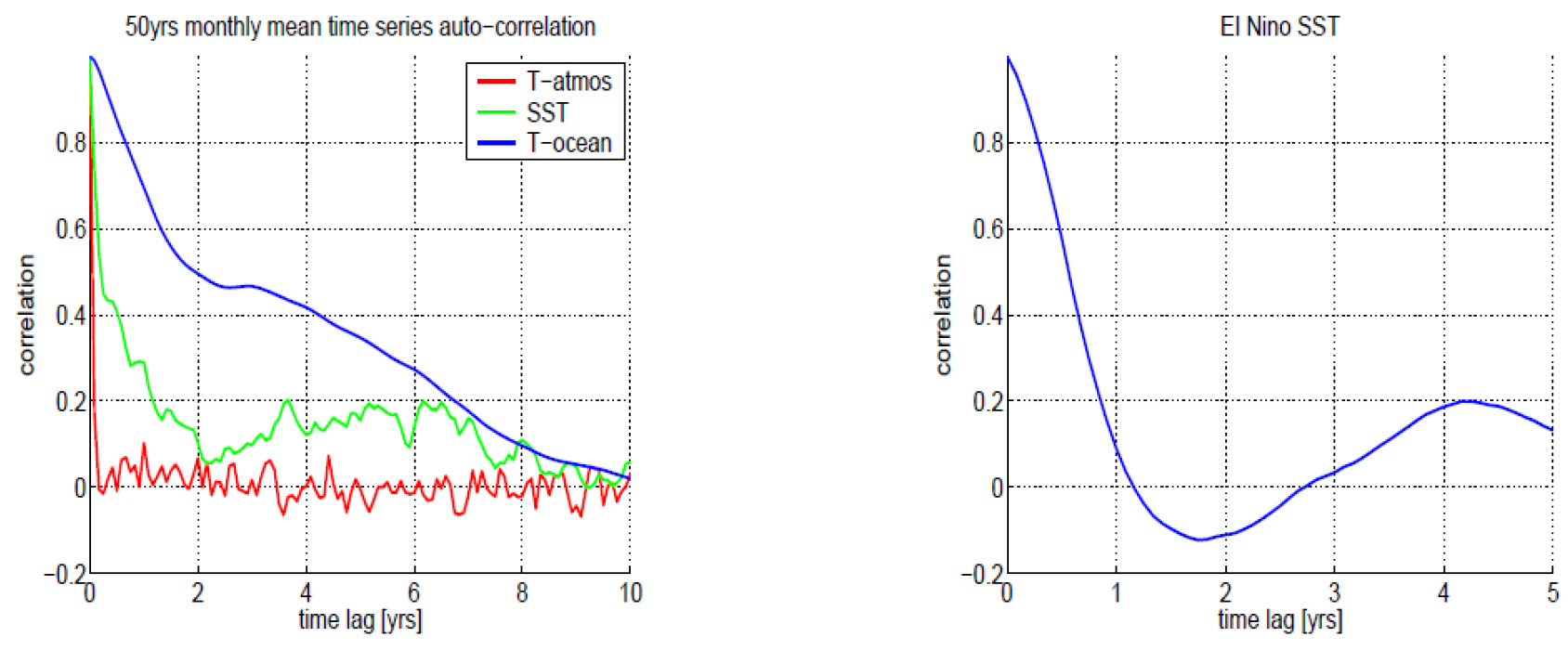

Auto-covariance function#

auto-covariance function \(\gamma\) describes the time scale behavior of a time series: how likely a variable depends on its own time series. an example of autocorrelation: if todays weather is warm there is a high likelyhood that tomorrows weather is also warm

non-parametric estimator of the auto-correlation function:

where \(\gamma(\tau)\) is the sample auto-covariance function, (covariance of X with itself at a time lag of \(\tau\))

characteristics of \(\gamma\):

\(\gamma\) is symmetric

\(\gamma(0) = Var(\mathbf{X})\)

\(\gamma(\tau) \leq \gamma(0)\)

\(|\rho(\tau)| \leq 1\)

\(\rho(\tau) < 0~\Rightarrow\) oscillation

\(\rho(\tau)\) illustrates how the dynamical system responds to a disturbance from the equilibrium, persistence of a forecast skill

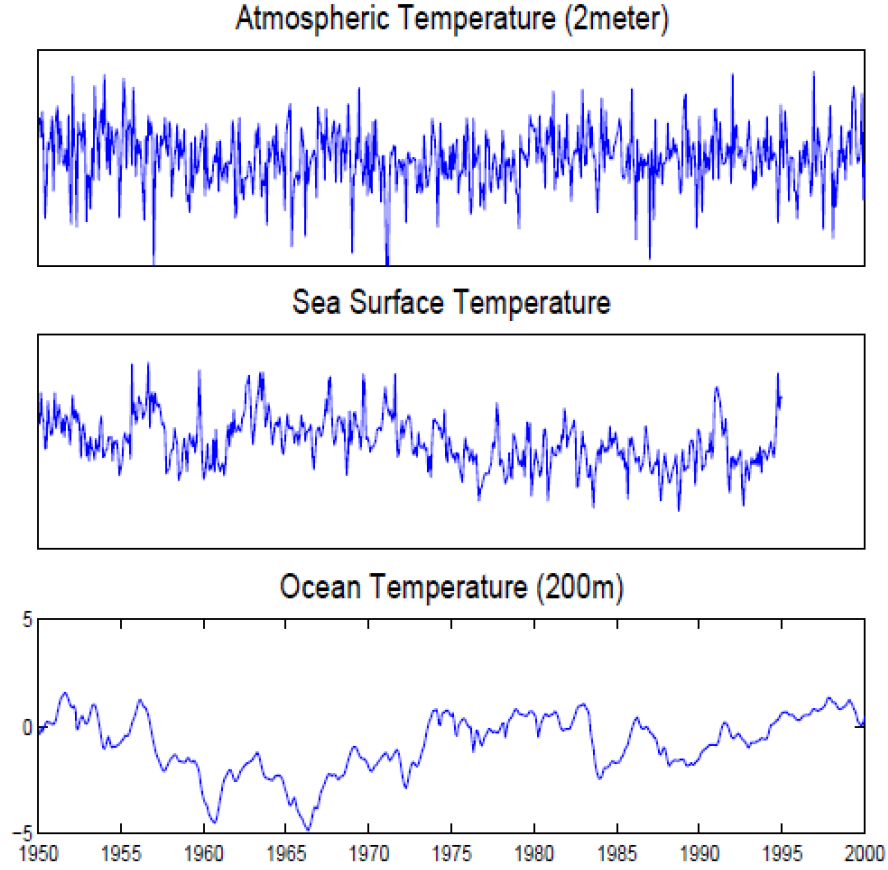

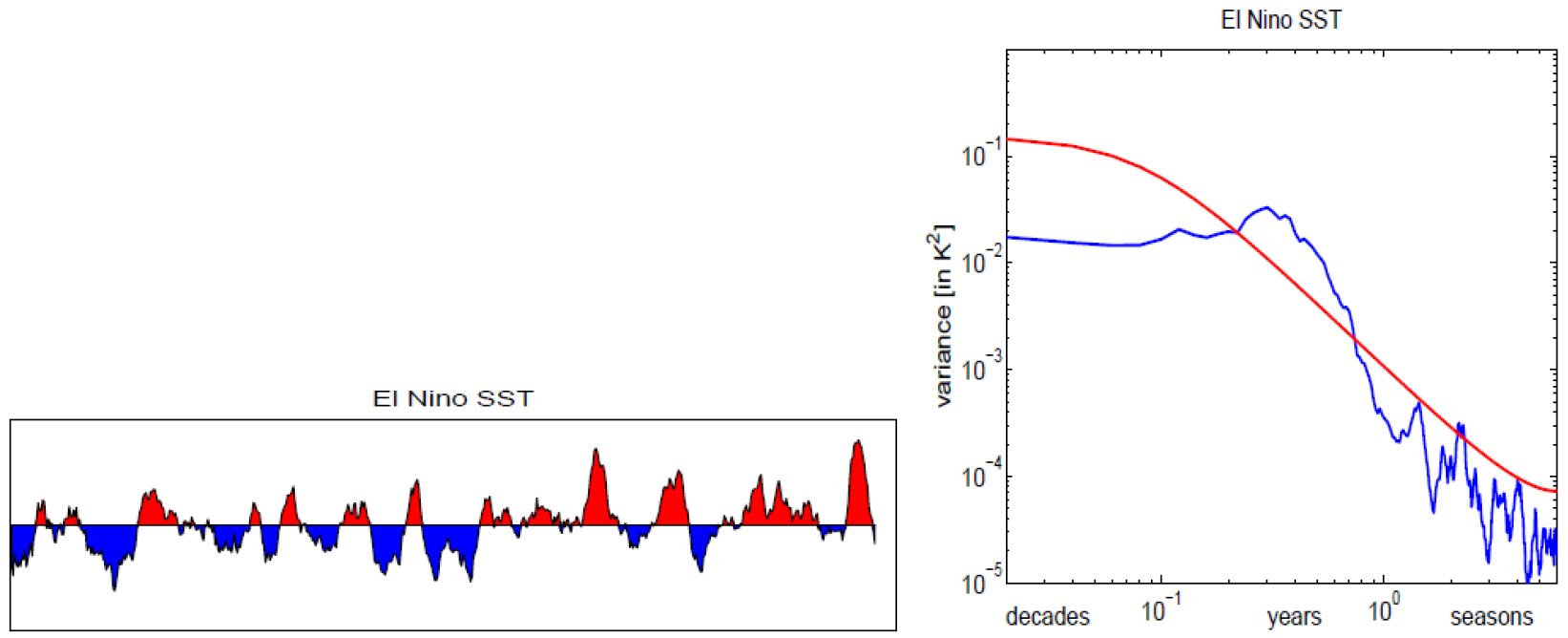

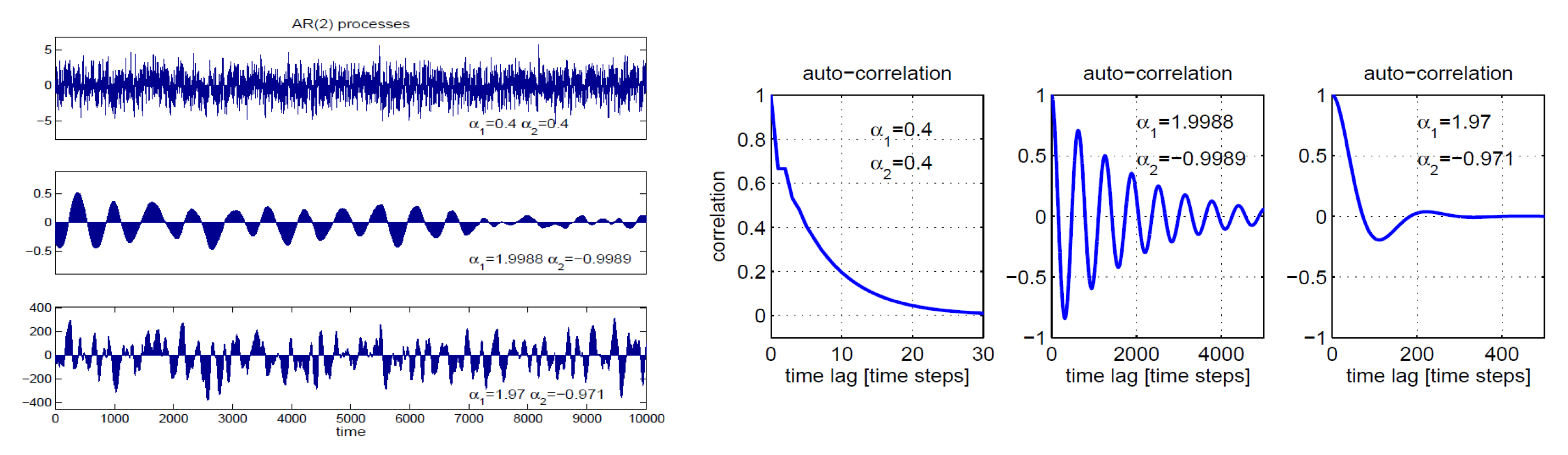

auto-correlation functions of the above time series in Figure 3 below

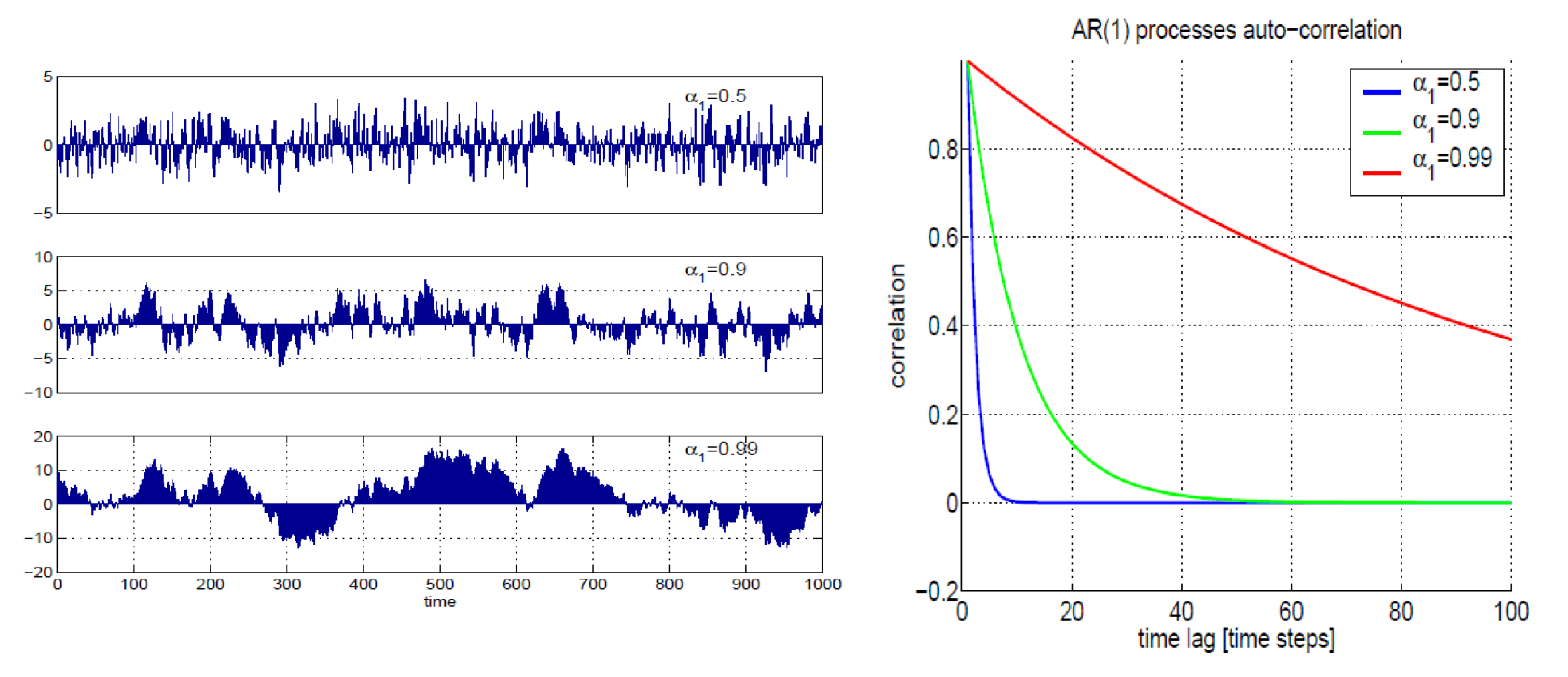

Autoregressive (AR) processes#

in an AR process each value in a time series is modeled as a linear combination of its previous values, along with some random noise. a general AR(p) process can be represented as follows:

\(\alpha_1,\alpha_2,...,\alpha_p\) - autoregressive coefficients determining the dependance on the past values,

\(\varepsilon_t\) - random error term or white noise at time \(t\)

order p of the autoregressive process determines how many past values have to be considered in the predicition of the current value

AR(1) processes rely only on the previous value

while AR(2) processes rely on the previous two values

Decorrelation time#

describes characteristic timescales of stochastic processes: how fast the autocorrelation decreases with time lag as a measure of the memory and persistence of the processes

number degree of freedom \(n_X\) of \(X\) (initially we had the definition for \(n_X\) that \(X_i\) and \(X_j\) have to be independent, meaning uncorrelated), central limit theorem:

relation between the true number of time steps used and \(n_X\) is the decorrelation time