Prof. Dr. Markus Meier

Leibniz Institute for Baltic Sea Research Warnemünde (IOW)

E-Mail: markus.meier@io-warnemuende.de

Stochastic climate models#

physical dynamical equation:

evolution in time is still unknown due to

not exactly known initial state (demonstrated by the Lorenz model): deterministic chaos

unknown time derivative (demonstrated by the Lorenz model)

unknown physical processes A

\(A\): slow dynamics

\(f_m, f_a\): fast dynamics, multiplicative, additive white noise

deterministic chaos: start with certain initial state and compute time evolution. now start from the same initial state with add small perturbation added - first similar time evolution but after some time the two paths diverge and develop totally different.

a white noise process is an uncorrelated time series of normally distributed random values, noise can generate low-frequency variability in X (Hasselmann, 1976), not only introduced by the external forcing (solar radiation, volcanoes)

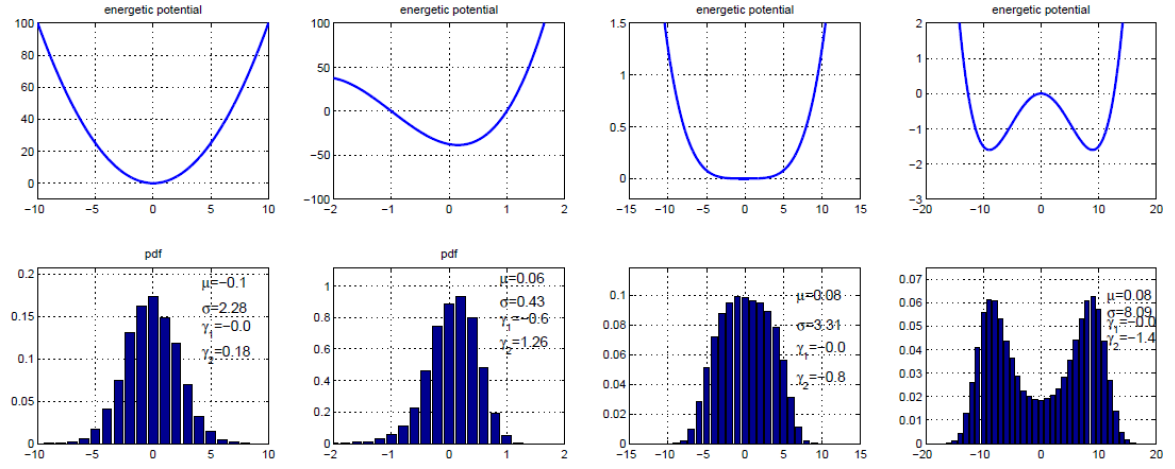

Pdf of some stochastic processes#

1. Linear damping model#

pdf is a normal distribution

potential and pdf shown in left column of Fig. 1

example: slab ocean model for the sea surface temperature (SST). change in SST for a constant height \(h\) depends on the atmospheric forcing:

while the atmospheric forcing is linearly dependent of the SST itself:

the time evolution of the SST is in the SST itself if the atmospheric temperature \(T_{atmos}\) is white noise. this is called an AR(1)-process (more about AR-processes later in this lecture)

2. Asymmetric feedback model#

pdf is skewed

potential and pdf shown in second to left column of Fig. 1

if the damping is stronger for deviations to the larger side of the equilibrium state than for deviations to the lower side, the pdf will be positively skewed and deviations to smaller values are more likey than deviations to larger values

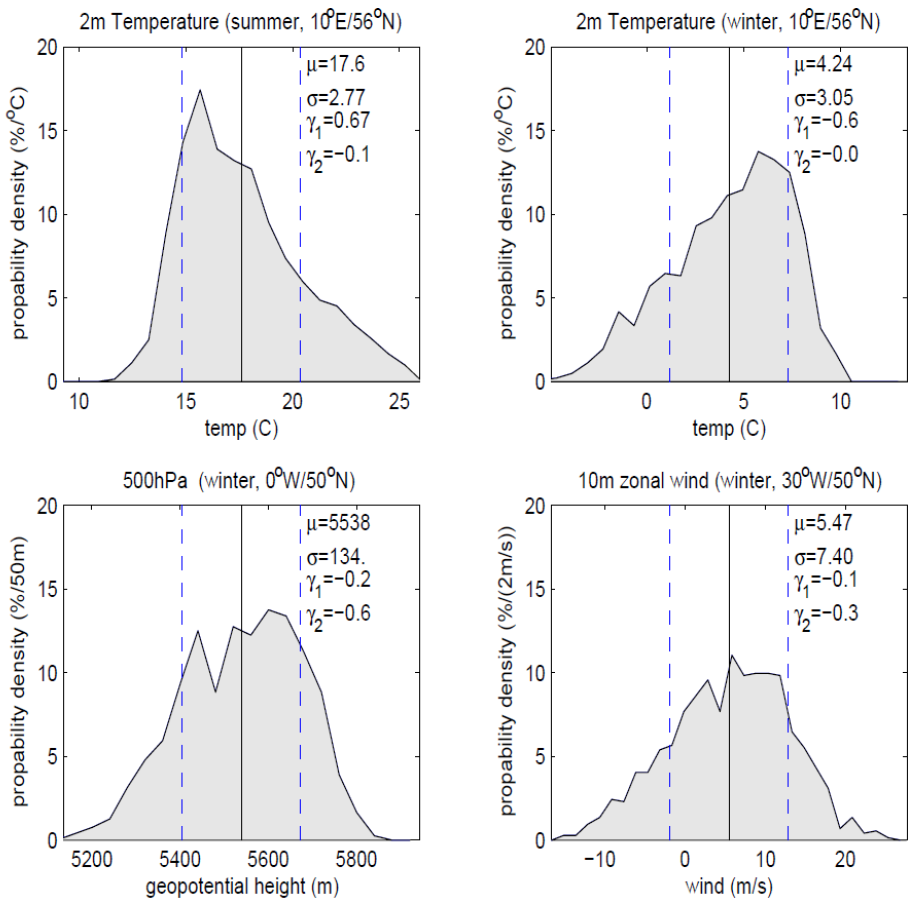

Fig. 2 shows the pdf of some exemplary advection variables

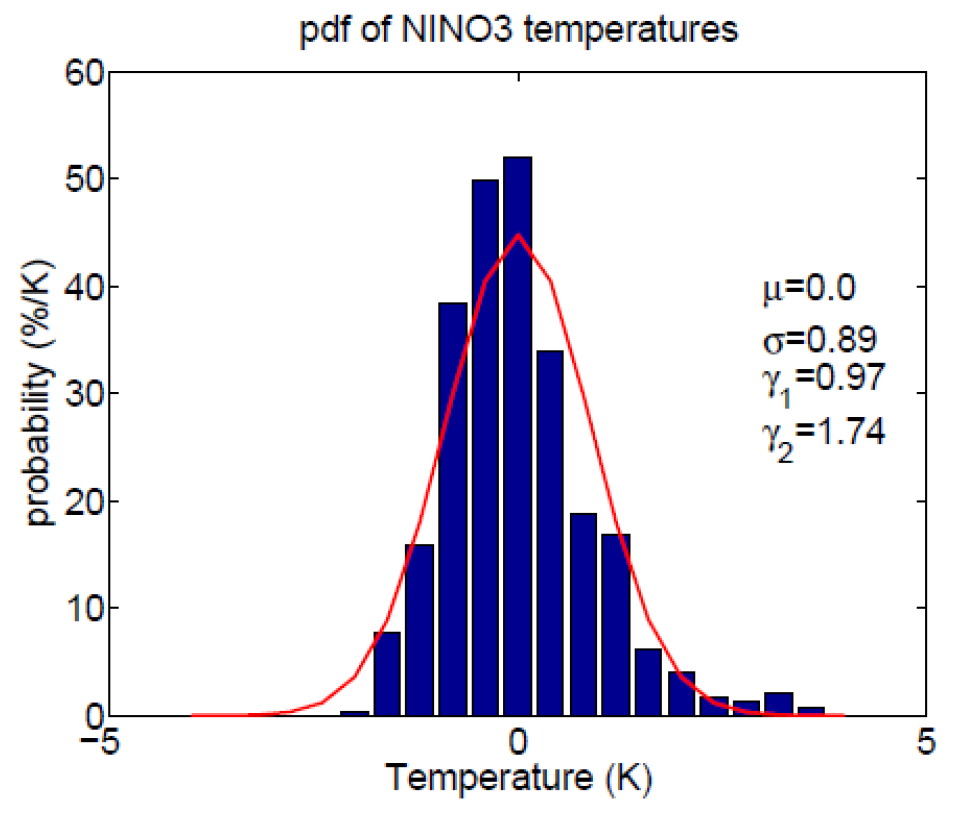

Fig. 3 shows the pdf of NINO3 temperatures

3. Non-linear damping model#

pdf with kurtosis

potential and pdf shown in second to right column of Fig. 1

non-linear but symmetrical damping, negative kurtosis causes a pdf which is less peaked than the Gaussian distribution

4. Non-linear model#

pdf is bimodal

potential and pdf shown in right column of Fig. 1

two equilibria caused by deterministic cycles (daily, annual), pdf of a sine function is bimodal

Autoregressive (Markov) processes#

dynamics of many physical processes can be approximated by first-, second-, or sometimes higher-order ordinary linear differential equations:

with \(z(t)\) deribing the external forcing. if the external forcing \(z(t)\) is a white noise process, then equation (31) defines an auto-regressive process of the second order, short AR(2)-process

time discretization for numerical implementation:

with the prefactors \(\alpha_1=\frac{a_1+2a_2}{a_0+a_1+a_2}\), \(\alpha_2=\frac{-a_2}{a_0+a_1+a_2}\) and \(\xi_t=\frac{1}{a_0+a_1+a_2}z_t\)

in general: \(\mathbf{X_t}:t \in \mathbb{Z}\) is an auto-regressive process of order p if there exists real constants \(\alpha_k~(k=0,1,...,p)\) with \(\alpha_k\) not equal to 0 and a white noise process \(\mathbf{Z_t}:t\in\mathbb{Z}\) such that:

analytically an AR(p)-process is described by:

we assume \(\mu=0 \Rightarrow \alpha_0=0\). variance of AR(p)-processes is given by:

with \(\rho_k\) the auto-correlation function of \(\mathbf{X_t}\):

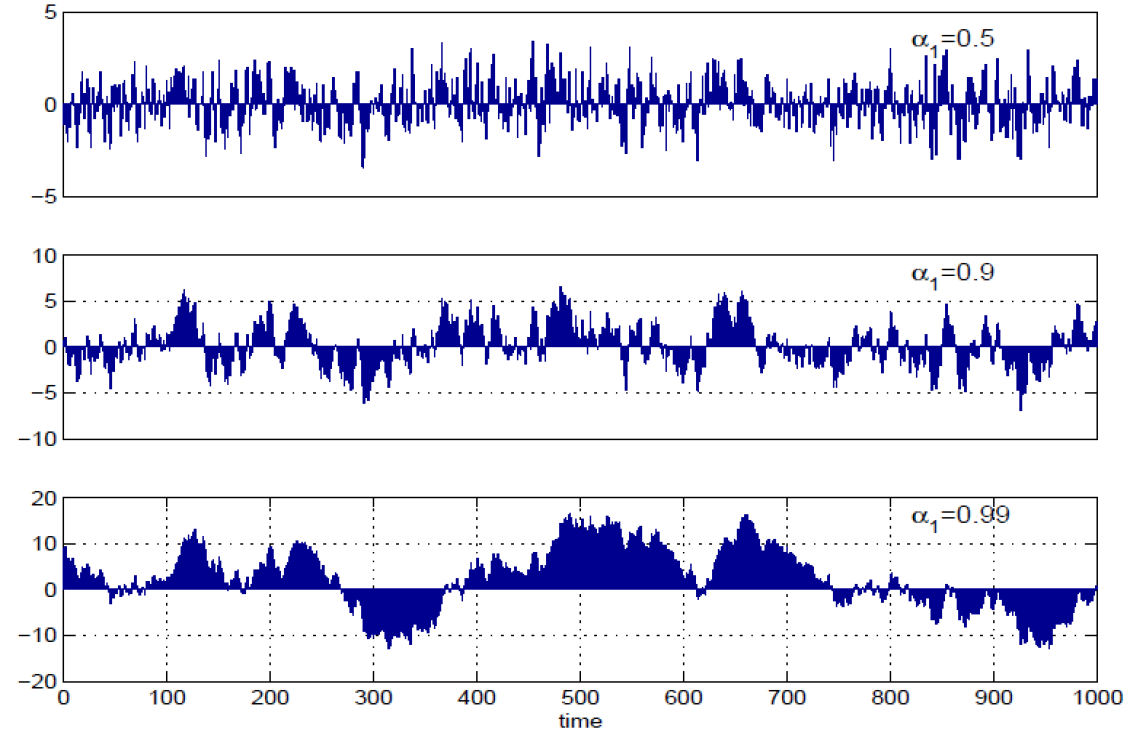

AR(1)-processes#

AR(1)-processes can be described by:

with a variance of

\(\rho_1 = \alpha_1\) lag(1) auto-correlation

with the damping parameter

noise generates low-frequency variability

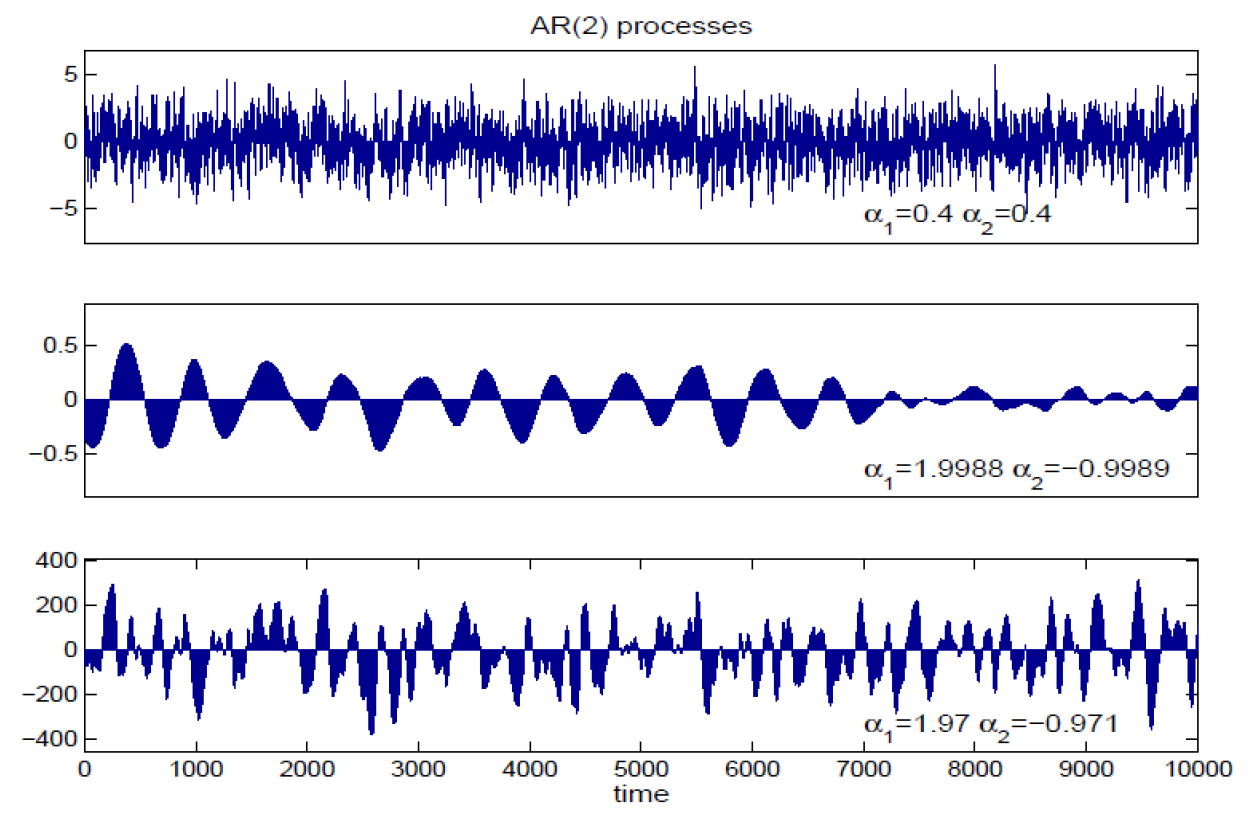

AR(2)-processes#

AR(1)-processes can be described by:

stationary:

AR(2)-process:

\(\alpha_2\) can only show oscillatory behavior if \(\alpha_2<0\)

damped oscillating system, which can, unlike the AR(1)-process, have a preferred time scale at which the system oscillates if driven white noise, e.g. El Nino Southern Oscillation